What Happens With Medicare When You Turn 65

Turning 65 is big milestone.

It comes with some new perks like travel discounts, hotel savings, and other benefits. But it also opens an important window for decisions about your health coverage.

The choices you make can carry long term financial consequences.

Some people are enrolled automatically. Others are not.

Some can delay enrollment without a penalty. Others need to enroll on time to avoid one.

What applies depends entirely on your situation.

Understanding your options before this window closes matters. It can help you avoid unnecessary costs, coverage gaps, and headaches down the road.

Understand Your Enrollment Window

Missing this window can trigger permanent penalties

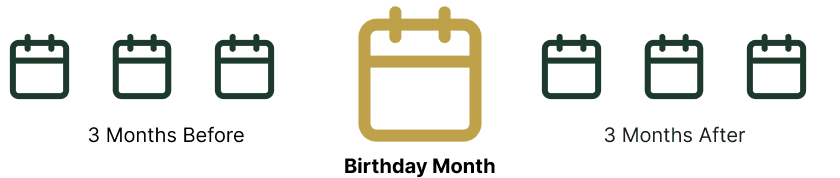

When someone turns 65, one of the first things I explain is their Initial Enrollment Period, or IEP.

It’s a seven month window. It starts three months before your 65th birthday, includes your birthday month, and continues for three months after.

This is your first opportunity to enroll in Medicare Part A and Part B without late enrollment penalties.

Here’s what most people don’t realize. The month you enroll determines the month your coverage starts.

If you enroll before your birthday month, your coverage typically starts the month you turn 65. If you wait until later in the window, your start date can be delayed.

If that window closes and you do not qualify for a Special Enrollment Period, there can be long term consequences. That can mean permanent late enrollment penalties, delayed coverage, and higher premiums for life.

The timing matters more than most people expect.

Do You Need to Enroll at 65?

You Likely Need to Enroll |

You May Be Able to Delay |

|---|---|

|

You do not have active creditable coverage |

You have active coverage through an employer |

|

You are retiring at or before 65 |

Covered under a spouse’s employer plan |

|

Your current coverage will end at 65 |

You have other qualifying creditable coverage |

Always verify that your coverage is considered creditable before delaying enrollment.

Not everyone needs to enroll in Medicare at 65. Your next step depends on the coverage you have right now.

Before deciding to delay enrollment, there are two things to confirm. Is your current coverage considered creditable under Medicare rules? When you turn 65, which coverage pays first and which pays second?

Getting this wrong can trigger lifetime late enrollment penalties or gaps in coverage. Understanding how your current coverage coordinates with Medicare is essential.

Common Medicare Mistakes

If You’re Approaching 65

Get It Right the First Time

If you are within six months of turning 65, this is the right time to review your options.

For official program details and updated cost information, visit Medicare.gov. Premiums, deductibles, and coverage rules can change from year to year, so reviewing current information matters.

Medicare explains the rules. I help you apply those rules to your situation.

Medicare is not just about enrolling. It is about setting your coverage up correctly for the years ahead.

If you want clarity before making a decision, I can help you:

- Confirm whether you need to enroll now

- Avoid lifetime penalties

- Compare your options correctly

- Estimate realistic annual cost exposure

- Enroll correctly the first time

When you set it up correctly from the start, you avoid expensive fixes later.